Back to the Basics: Revisiting an Enduring Strategy

In a recent email from a very well-known firm in our industry, the subject line stated, ‘[this person] Shares A New Retirement Strategy.’ Always eager to add a new tool to the toolbox, I read further. What the article was sharing was a strategy that isn’t ‘New’, but it’s one that we’ve been using since the day Elevated Retirement Group’s doors opened. What were they describing? Bucketing. Specifically, using a three-bucket investing strategy to allocate assets to ensure that risk was being well-managed and income would last for the duration of a person’s (or couple’s) retirement. So while this author wasn’t offering anything new, let’s use this as an opportunity to revisit the very basics of this bucketing strategy.

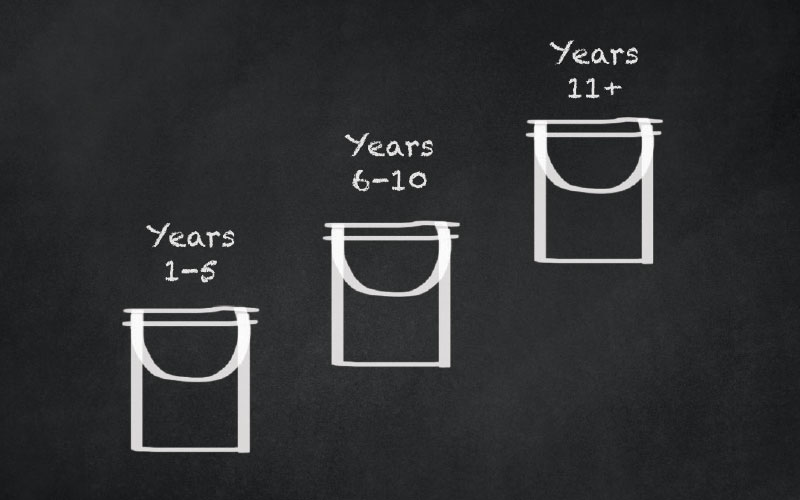

What is bucketing? Bucketing (also called age-banding) can be defined as an approach to developing retirement income that segments retirement assets by category. While categories may be based on risk level of certain assets, the buckets can also be segmented by time periods designed to cover the life-span of the retiree. An example is a 3-bucket plan, with bucket 1 designed to cover years 1-5 of retirement, bucket 2 earmarked for years 6-10, and bucket 3 covering years 11+.

Bucketing, as compared to other methods of retirement income planning is a safety-first approach. Bucketing can provide substantial psychological benefits to retirees by using age-based buckets in sequence. This allows a retiree to pair investments of increasing risk or guaranteed return with the time segment that best matches the chosen investment or product. Put another way, the money that needs to be available first during retirement should be placed into the first bucket, while money that won’t be needed for many years to come is placed in the second or third buckets.

Offering pension-like income certainty, bucketing has the added benefit of breaking the long time horizon of retirement into smaller segments. Bucketing allows you to utilize several smaller investment or product allocations in age-banded buckets. That way, if the markets change dramatically, the assets placed in the buckets can be adjusted to respond. It’s a form of diversification that also pairs products more closely with expected timeframes of use.

There are a number of ways to fund the buckets. For example, you can invest increasingly risky assets in each successive bucket. Or, you can build the entire income plan in a guaranteed manner by using 5-year payout annuities in the first two buckets, with a lifetime income rider annuity product in the third bucket, allowing the strongest guaranteed growth of income benefits. With either direction the retiree chooses – the risk-based bucketing strategy or one of the many guaranteed options – if the retiree’s needs change, there is still flexibility available to change the future buckets. If the retiree(s) passes away before ‘turning on’ the income from all the buckets, any remaining account balances will pass to heirs, thus avoiding the premature death risk of some other strategies.

By pairing the retirement income needed with the income derived from the bucket plan, any remaining ‘extra’ money is freed-up from income generation duties and is able to remain at-risk in the stock and bond markets for purposes of discretionary wants, inflation protection, long term care needs, and giving.

With these extra discretionary investment assets, the principles of prudent investing still apply, but the need for those assets to generate consistent income has been removed, thanks to the income generated by the buckets.

What are the downsides to bucketing? For one, the multi-bucket approach can be a bit more complex than other models that use a single source of income. Bucketing also requires a broader access to products in order to build it effectively.

What are the downsides to bucketing? For one, the multi-bucket approach can be a bit more complex than other models that use a single source of income. Bucketing also requires a broader access to products in order to build it effectively.

Generally, no single insurance company or investment manager will offer the most competitive options for all the buckets. Bucketing tends to work best with a combination of guaranteed income products and risk-based investments, so dually-licensed advisors can have an advantage when building a bucketed plan.

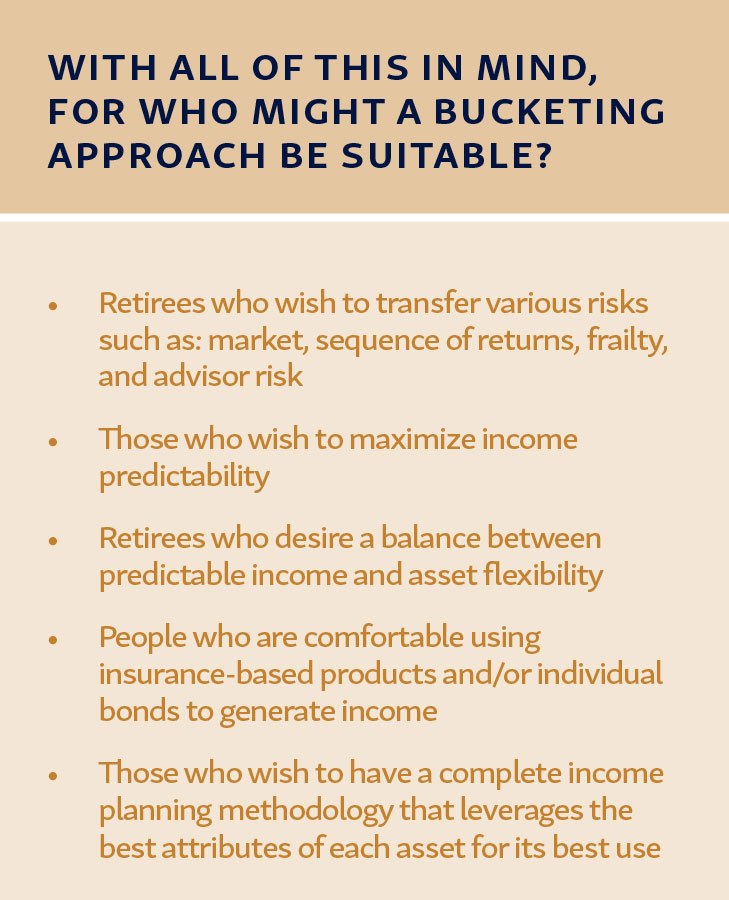

While this discussion was never intended to be an exhaustive analysis of bucketing, I hope it inspires you to learn as much as possible before committing your retirement assets to an income planning strategy. As a safety-first approach, bucketing offers a lot of flexibility for those families who wish to provide certainty and reliability of income.

In an era of ever-increasing complexity and retiree lifespans, retirees face an unprecedented responsibility to plan their retirement income prudently. Bucketing is a strategy we’ve been very comfortable with, long before it was declared as ‘New’ again.